How to reduce your corporation tax

Posted on 30th April 2020

Business owners often operate through a limited company in order to legally reduce the amount of tax they have to pay. As responsible business owners, it's important to ensure that you're paying the correct amount of tax - while making sure you don't pay more than you are obliged to by law. After all, who would say no to keeping more of their well-earned profits?

The corporation tax rate for company profits in 2020/21 is 19% - the same as the 2019/20 tax year. This means that a business will pay 19% of their annual profits in corporation tax. A company making £100,000 in profits will pay £19,000 in corporation tax, for example. While it seems pretty straightforward, you must remember that this is tax. And as ever, tax is far from a straightforward topic.

As mentioned, corporation tax is calculated on profits - not on sales or turnover.. This means there are two key components to consider: sales and expenses. The key to reducing your company's corporation tax liability is therefore to check that all your sales and expenses are correct. Easy, right?

We've put together nine effective ways you can ensure you're not paying too much corporation tax. Please note that tax is a complex subject (as if you need telling!) and every company's situation is different. There may be allowances or deductions for your specific industry or sector, so please, as always, take this information as very general advice.

You should always speak to a tax expert for tailored advice and support - we're more than happy to help!

Here are a few basics every company director should know to ensure they’re not paying more tax than they need to...

1. Check sales are not overstated

This is why you should ensure your bank reconciliations are up to date. Are there any invoices you raised in error or jobs that didn't come to pass? What about bad debts? Don't have a bookkeeper? Hire one!

2. Check you're taking the correct directors salary from the company

Your accountant (hopefully us!) will be able to confirm the salary you should be withdrawing every month. Salary is a valid tax deductible business expense and therefore reduces the profit and corporation tax. Our blog post here can help you work out what you should be taking every month.

3. Check you've claimed all valid business expenses

It literally pays to stay on top of your expenses. Say you're paying £7,500 over the course of the tax year for equipment, insurance, travel and professional fees, but you forget to claim the capital allowance you're entitled to, your profits could be overstated by £7,500! This means you'll end up paying an extra £1,425 in corporation tax which you could have kept for yourself. It's not to be sniffed at! Our free and downloadable expenses guide here can help you figure out what you can claim for and save you money.

4. Time your equipment purchases

If you carefully plan any purchase of equipment, tools or vehicles so that you're timing them in a tax-efficient manner, you could save money. If you are considering a purchase, aim to purchase before your year-end to ensure you get that tax relief as soon as possible. For example, if you're planning tp buy a van and your company year ends on 31st March, if you buy the van before 31st March, your next corporation tax bill will be reduced. If you purchase the van on 1st or 2nd April, for example, you won't see a tax reduction until the following year.

5. Claim your work-from-home costs

If you’re working from home, your company can repay you for some costs associated with running the business. You can claim either the basic allowance - up to £4 per week (or £18 per month) without having to itemise or justify the costs to HMRC. This basic allowance is designed to acknowledge you writing up business notes, invoices and general ad-hoc administrative tasks at home.

Alternatively, you can claim for the apportioned cost. This is for people who work from home at least one full day per week, and have dedicated office space in their home. The amount you can claim will depend on proportion of the area of the house is used for business, how often the area for is used for business and how long for, plus the costs you can attribute or apportion to this business usage. The costs you can proportion are mortgage interest (excluding repayment element), rent, water, gas and electricity. You may also be able to claim a proportion of your landline and broadband costs. If you choose to use the apportioned method, you’ll need to ensure you can prove that you have a functional work space that’s used exclusively for business. You’ll also need to be able to provide evidence of your calculations to a HMRC inspector, if requested.

6. Pay into a company pension

Any contributions paid into a company's pension scheme for directors and employees qualify for 100% tax. We, along with our personally recommended financial advisors, can provide more detailed information. Check out our blog post here about the benefits of pensions for limited company directors, and to learn more about the schemes available.

7. Make sure your mobile phone contract is in the company name

The vast majority of small business owners will have one mobile phone for both business and personal use. The purchase of the handset and cost of the line rental and calls can only be paid for and treated as tax-deductible in full if the handset and contract is in the company name, the company pays the costs directly (not reimbursing the director/staff member) and the phone is primarily used for business use, with minimal/incidental personal use. It's important to note that if the mobile contract is in your (the director’s) name, and you pay for it personally, strict rules by HMRC state that you can only claim the cost of business calls based on an itemised bill, and no proportion of line rental.

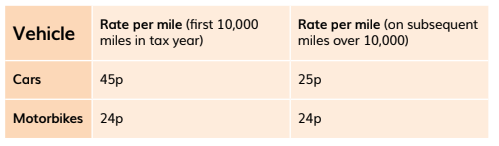

8. Check you've claimed any business mileage

You can claim business mileage from your limited company when driving your own car for business purposes. Here’s a table of rates for 2020/21:

9. Get tax-free income protection cover

Many business owners are unaware that they may be able to put life insurance through the company as a legitimate tax-deductible business expense. Not only that, if the policy meets certain conditions, it is not treated as a benefit-in-kind so there is no National Insurance or personal tax payable. Win, win! However, it's important to note that it is only tax-deductible if 1) it only provides life cover and no other benefits; 2) it only pays out a lump sum if the director/employee dies in service before the age of 75; 3) it doesn't have a surrender value and 4) it can only pay out to an individual or charity. If you'd like us to put you in touch with one of our trusted financial advisors, please feel free to get in touch.

Next steps

Feel free to get in touch with us today to see how we can ease your tax and accounting headaches. It's so important to ensure that you're keeping as many pennies from each pound as possible, it really can pay dividends. Feel free to give us a call or drop us an email. We’ll be more than happy to help advise you, taking your individual circumstances into consideration.

Written by

Nicola J Sorrell -

Effective Accounting

Founder | Xero Champion | IR35 Expert

Share this post: